Southeast Asia smartphone value rises as shipments stall

Tue, 17th Mar 2026

Southeast Asia's smartphone market recorded shipment growth of 0.7% in 2025, according to IDC.

Market revenue rose 11.3% as buyers shifted towards higher-priced devices.

IDC's latest quarterly mobile phone tracker showed a widening gap between unit growth and market value after the region passed 100 million smartphone shipments in 2024. The figures suggest vendors are relying less on volume expansion and more on pricing and product mix to support returns.

Value shift

The clearest trend in 2025 was the divergence between shipment volumes and sales value. Devices priced at USD $200 and below declined 5.7% year on year, though lower-priced handsets still accounted for more than 60% of the region's smartphone market.

This left Southeast Asia exposed to cost pressures in the budget segment while also highlighting a steady shift in demand towards mid-range models. Vendors increasingly pushed pricier handsets as consumers upgraded within the middle tier.

"Despite minimal YoY volume growth in ASEAN in 2025, the market's total value increased by 11.3% YoY. Shipments of smartphones priced at $200 and below declined by 5.7% YoY. This trend indicates a gradual shift in consumer demand toward mid-range smartphones, contributing to overall market value growth despite limited unit growth," said Phang Hoon Yik, research analyst at IDC.

Vendor rankings

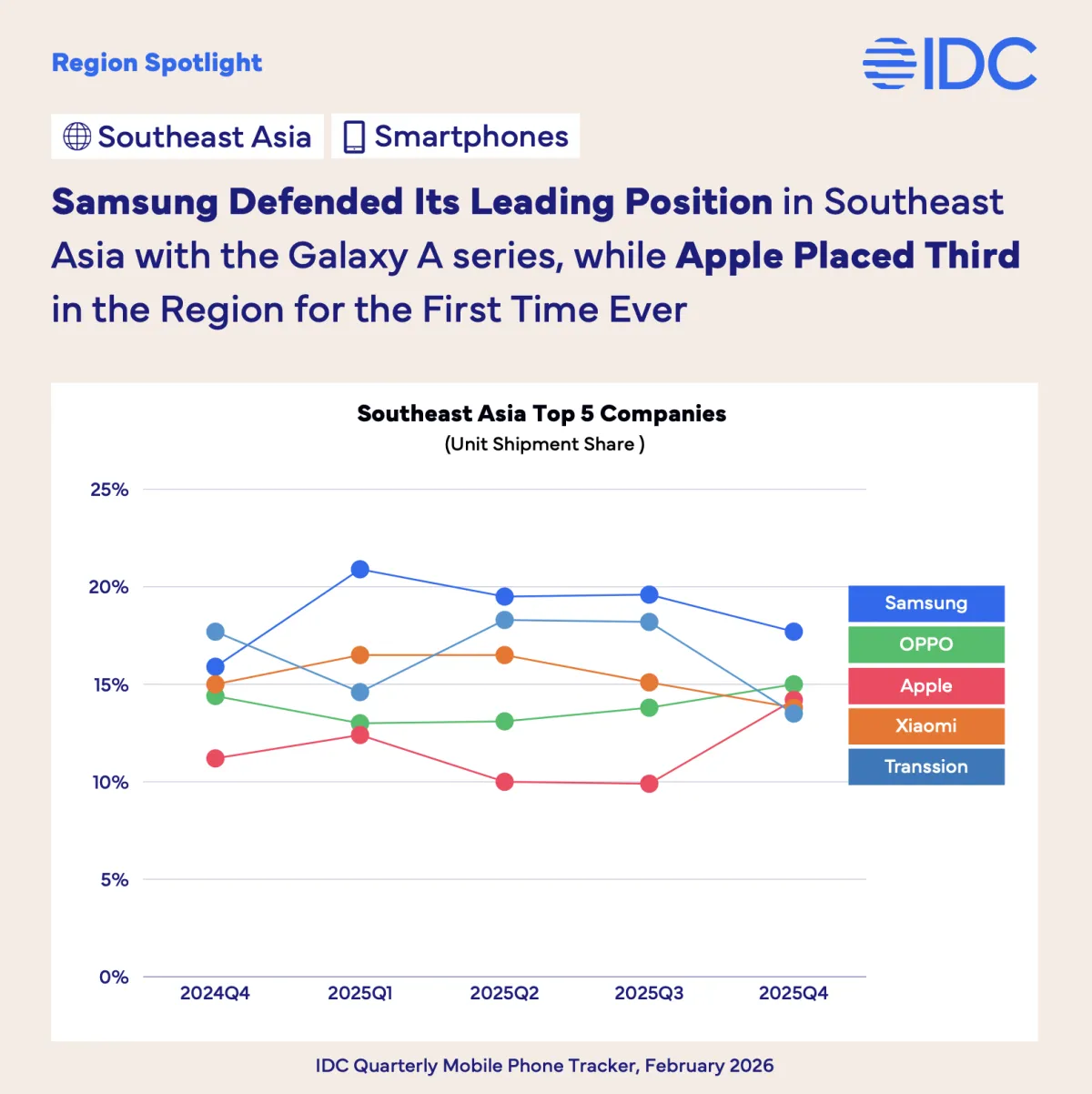

Samsung retained the top position in Southeast Asia, helped by demand for its Galaxy A-series devices. Apple rose to third place in the region for the first time, reflecting stronger sales in higher-income markets.

Country-level rankings were more uneven. Samsung ranked among the top three vendors in every major Southeast Asian market and led annual share in Singapore, Malaysia, Thailand and Vietnam.

Apple's strongest gains came in Singapore and Thailand. It also expanded in Vietnam and the Philippines in the fourth quarter, in line with the broader shift towards more expensive smartphones.

Chinese brands remained dominant in entry-level categories. Transsion led in the Philippines and Indonesia, while Xiaomi, OPPO and vivo retained significant shares across much of the region.

Pricing pressure

Component costs played a larger role in vendor planning during the year. Rising memory costs and supply shortages forced smartphone makers to rethink pricing, launches and portfolio structure.

Some brands introduced new models at higher prices, while others focused on premium lines or cut the number of lower-margin products. The result was fewer low-cost launches in several countries and greater emphasis on mid-range models.

"Vendor strategies varied across the region, as they responded to escalating memory costs and shortage, with some vendors launching new models with pre-emptive price hikes while others pushed higher-end lines and streamlining portfolios to focus resources," said Angela Medez, senior research analyst at IDC.

These moves helped vendors protect revenue, but they also weighed on shipment growth in more price-sensitive markets. The effect was most visible where demand remained concentrated in low-cost handsets.

Country variation

Performance differed widely across Southeast Asia in 2025. The Philippines posted the strongest annual shipment growth at 2.9%, supported by ongoing demand for entry-level devices, although momentum slowed in the final quarter.

Singapore and Thailand also recorded annual growth, driven by stronger premium sales. By contrast, Indonesia and Vietnam saw flat or falling volumes as vendors cut shipments of lower-priced devices.

Fourth-quarter figures pointed to broader weakness across the region. Several markets contracted as brands limited supply and adjusted inventories in response to changing cost conditions.

2026 outlook

IDC expects tighter market conditions in 2026 as memory shortages raise costs and reduce product availability, especially in the budget segment. With more than 60% of the regional smartphone market still priced below USD $200, the impact could be significant for both vendors and consumers.

The fourth quarter of 2025 may have been an early sign of deeper pressure ahead.

"4Q25 was just a mild precursor to what we will start to see in 2026, as memory chip shortages rage, driving up costs and tightening product availability. This is expected to hit the ASEAN region hard, with the overall smartphone market projected to drop sharply. The sub-$200 segment, which accounts for over 60% of the regional market, is likely to see the greatest impact," said Vanessa Aurelia, research analyst at IDC.